The default position of 18F when developing new projects is to:

1. Use Free and Open Source Software (FOSS), which is software that does not charge users a purchase or licensing fee for modifying or redistributing the source code, in our projects and contribute back to the open source community.

2. Create an environment where any project can be developed in the open.

3. Publish publicly all source code created or modified by 18F, whether developed in-house by government staff or through contracts negotiated by 18F.

Eric Mill and Raphael Majma published a post on Tumblr that explained what FOSS, the policy, 18F’s open source team, approach and teased forthcoming guidelines for reuse:

FOSS is software that does not charge users a purchase or licensing fee for modifying or redistributing the source code. There are many benefits to using FOSS, including allowing for product customization and better interoperability between products. Citizen and consumer needs can change rapidly. FOSS allows us to modify software iteratively and to quickly change or experiment as needed.

Similarly, openly publishing our code creates cost-savings for the American people by producing a more secure, reusable product. Code that is available online for the public to inspect is open to a more rigorous review process that can assist in identifying flaws in the source code. Developing in the open, when appropriate, opens the project up to that review process earlier and allows for discussions to guide the direction of a products development. This creates a distinct advantage over proprietary software that undergoes a less diverse review and provides 18F with an opportunity to engage our stakeholders in ways that strengthen our work.

The use of open source software is not new in the Federal Government. Agencies have been using open source software for many years to great effect. What fewer agencies do is publish developed source code or develop in the open. When the Food and Drug Administration built out openFDA, an API that lets you query adverse drug events, they did so in the open. Because the source code was being published online to the public, a volunteer was able to review the code and find an issue. The volunteer not only identified the issue, but provided a solution to the team that was accepted as a part of the final product. Our policy hopes to recreate these kinds of public interactions and we look forward to other offices within the Federal Government joining us in working on FOSS projects.

In the next few days, we’re excited to publish a contributor’s guide about reuse and sharing of our code and some advice on working in the open from day one.

“The consumer experience shared in the narrative is the heart and soul of the complaint,” said CFPB Director Richard Cordray, in a statement. “By publicly voicing their complaint, consumers can stand up for themselves and others who have experienced the same problem. There is power in their stories, and that power can be put in service to strengthen the foundation for consumers, responsible providers, and our economy as a whole.”

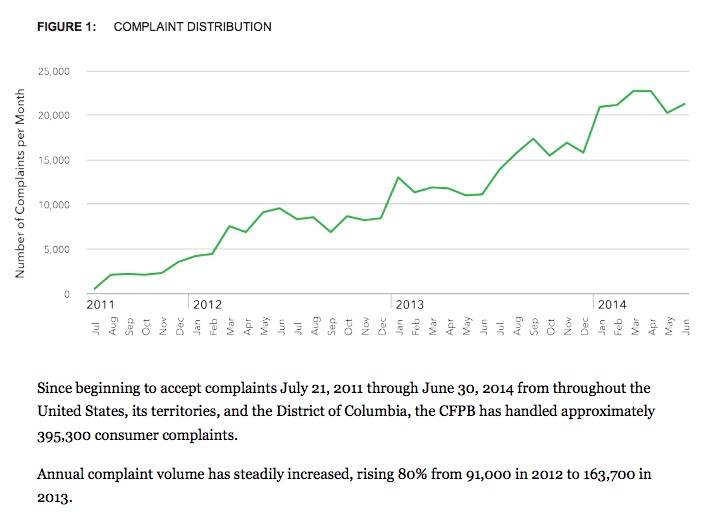

The CFPB was given authority and responsibility for handling consumer complaints regarding financial services by the Dodd-Frank Wall Street Reform and Consumer Protection Act, more than three years ago. Today, the CFPB released an overview of the complaints that the agency has handled since July 21, 2011,

Today, the CFPB released an overview of complaints handled since the Bureau opened on July 21, 2011. (The graphics atop this post and below are sourced from this analysis.) According to the data inside, up until June 30, 2014, the CFPB has handled approximately 395,300 consumer complaints.

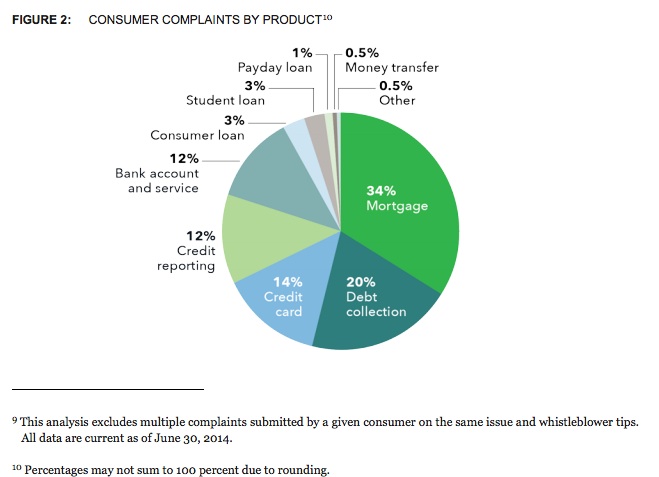

According to the overview, the World Wide Web has been a key channel for people to file complaints to the CFPB: 56% of all consumer complaints were submitted through the CFPB’s website. 10% were submitted via telephone calls, with the balance coming in through mail, email, and fax. The rest of the report contains tables and data that breaks down complaints by type, actions taken, company responses, and consumers’ feedback about company responses.

By releasing these narratives, not just the number of complaints, the agency holds that the following benefits will accrue: more context to the complaint, specific trends in complaints, enabling consumers to make more informed decisions, and spurring competition based on consumer satisfaction. In the release announcing the proposed policy, the CFPB emphasized that consumers must opt-in to share these stories: “The CFPB would not publish the complaint narrative unless the consumer provides informed consent. This means that when consumers submit a complaint through consumerfinance.gov, they would have to affirmatively check a consent box to give the Bureau permission to publish their narrative. At least initially, only narratives submitted online would be available for the opt-in.”

Consumers could subsequently decide to withdraw their consent, resulting in the regulator removing the complaint from their website. Companies will be given the opportunity to publish a written response to the complaints that would appear next to a given consumer’s story.

The agency’s proposal states that “no personal information will be shared, stating that “complaints would be scrubbed of information such as names, telephone numbers, account numbers, Social Security numbers, and other direct identifiers.”

Getting that right is important — watch for powerful financial companies, their lobbyists and sympathetic politicians to raise privacy concerns about the proposal in DC in the weeks to follow.

While it may not be apparent at first glance, however, the collection and publication of these complaints would have an important, tacit effect upon the market for financial services. By collecting, structuring and releasing consumer complaints as data, the CFPB could add crucial business intelligence into the marketplace for these services. This isn’t a novel model: the Consumer Product Safety Commission already discloses a public complaint database at SaferProducts.gov, enabling merchants and services like Consumer Products to give people crucial information about their purchases. The SEC and FINRA would be well-advised to release financial advisor data in a similar fashion. Someday, complaints submitted from mobile e-patients may have similarly powerful corrective effect in the market for health care goods and services.

Last November, I speculated about the potential of a” kernel of a United States Digital Services team built around the DNA of the CFPB: digital by default, open by nature,” incorporating the skills of Presidential Innovation Fellows.

As I wrote last week, after a successful big fix to Healthcare.gov by a trauma team got the trouble marketplace for health insurance working, the Obama administration has been moving forward on information technology reforms, including a new development unit within the U.S. General Services Administration.

This week, that new unit became a real entity online, at “18F.

You know the UK’s awesome Government Digital Service? There’s a startup within the US gov’t to do the same work. https://t.co/yD1aZkIlOU

— Waldo Jaquith (@waldojaquith) March 12, 2014

As with the United Kingdom’s Government Digital Services Team, 18F is focused on delivery, an area that the UK’s executive director of digital, Mike Bracken, has been relentless in pushing. Here’s how 18F introduced itself:

18F builds effective, user-centric digital services focused on the interaction between government and the people and businesses it serves. We help agencies deliver on their mission through the development of digital and web services. Our newly formed organization, within the General Services Administration, encompasses the Presidential Innovation Fellows program and an in-house digital delivery team.

18F is a startup within GSA — the agency responsible for government procurement — giving us the power to make small changes with big effect. We’re doers, recruited from industry and the most innovative corners of public service, who are passionate about “hacking” bureaucracy to drive efficiency, transparency, and savings for government agencies and the American people. We make easy things easy, and hard things possible.

“Commencing countdown, engines on!” Meet 18F — a new way of delivering government services. http://t.co/UQD6ViA1FB

The 18F team, amongst other things, has some intriguing, geeky, and even funny titles for government workers, all focused around “agents.” API Agent. Counter Agent. Free Agent. Service Agent. Change Agent. User Agent. Agent Schmagent. Reagent. Agent onGover(). It’s fair to say that their branding, at minimum, sets this “startup in government” apart.

So does their initial foray into social media, now basic building block of digital engagement for government: 18F is on Twitter, Tumblr and Github at launch.

Looks like their office suite is pretty sweet, too.

This effort won’t be a panacea for federal IT ills, nor will a U.S. Government Digital Office nor the role of a U.S. chief technology officer be institutionalized until Congress acts. That said, 18F looks like a bonafide effort to take the approaches to buying, building and maintaining digital and Web services that worked in the Presidential Innovation Fellows program and the Consumer Financial Protection Bureau and trying to scale them around the federal government. The team explained more at their Tumblr blog about how they’ll approach their sizable remit:

Partner with agencies to deliver high quality in-house digital services using agile methodologies pioneered by top technology startups.

Rapidly deploy working prototypes using Lean Startup principles to get a desired product into a customer’s hands faster.

Offer digital tools and services that result in governmentwide reuse and savings, allowing agencies to reinvest in their core missions.

We’re transparent about our work, develop in the open, and commit to continuous improvement.

More than five years ago, Anil Dash wrote that the most interesting startup of 2009 was the United States government. Maybe, just maybe, that’s become true again, given the potential impact that the intelligent application of modern development practices could have on the digital government services that hundreds of millions of Americans increasingly expect and depend upon. What I’ve seen so far is promising, from the website itself to an initial pilot project, FBopen, that provides a simple, clean, mobile-friendly interface for small businesses to “search for opportunities to work with the U.S. government.”

Clay Johnson, a member of the inaugural class of Presidential Innovation Fellows and founder of a startup focused on improving government IT procurement, offered measured praise for the launch of 18F:

Is it a complete solution to government’s IT woes? No. But, like RFP-IT and FITARA, it’s a component to a larger solution. Much of these problems stem from a faulty way of mitigating risk. The assumption is that by erecting barriers to entry – making it so that the only bets to be made are safe ones – then you can never fail. But evidence shows us something different: by increasing the barriers to competition, you not only increase risk, you also get mediocre results.

The best way for government to mitigate risk is to increase competition, and ensure that companies doing work for the citizen are transparently evaluated based on the merits of their work. Hopefully, 18F can position itself not only as a group of talented people who can deliver, but also an organization that connects agencies to great talent outside of its own walls. To change the mindset of the IT implementation, and convince people inside of government that not only can small teams like 18F do the job, but there are dozens of other small teams that are here to help.

Given the current nation-wide malaise about the U.S. government’s ability to execute on technology project, the only approach that will win 18F accolades after the launch of these modern websites will be the unit’s ability to deliver more of them, along with services to support others. Good luck, team.

When 18F starts hiring, you’re going to want to drop everything to work there. https://t.co/yD1aZkIlOU

Many questions about the future of the agency remain (Wall Street and Republicans have not been sparing offering criticism over the past year) but credit where credit is due: the new consumer bureau has been open to ideas about how it can do its work better. This approach is what led New York Times personal finance columnist Ron Lieber to muse last week that “its openness thus far suggests the tantalizing possibility that it could be the nation’s first open-source regulator.”

It’s extremely rare that an agency gets built from scratch, particularly in this economic and political context. It’s notable, in that context, that the 21st century regulator has embraced many of the principles of open government in leveraging technology to stand up the Consumer Financial Protection Bureau. Elizabeth Warren, the architect of the agency, spoke to how open government, citizens and technology factor into the bureau’s work earlier this year:

Better government by design

Open government isn’t just about first principles for accountability, open data, social media, transparency, cultural change, citizen participation, innovation or feedback loops, however, though all of those factors matter. As the work of Code For America has shown this year, design matters in open government. Better citizen experience, communication and customer service depends on better design.

Lois Beckett aptly connected how the dots about why design matters to the CFPB’s work this week at ProPublica, where she wrote about the challenges the innovative financial regulator faces as it starts up.

…as the political battle rages on and media scrutiny focuses on Elizabeth Warren’s political future, little attention has been given to what the bureau has actually done. And its initial efforts are interesting, especially because they show a commitment to open government and real public engagement. (Ron Lieber noted that its blog actually accepts comments—”unlike, say, the White House’s.”)

The bureau’s mission is to create transparency in an industry dominated by confusing claims and mouse print. Good design isn’t just a perk here—it’s fundamental to the bureau’s regulatory efforts.

Case in point: One of the CFPB’s top priorities has been streamlining the federally required mortgage disclosure documents. If that sounds like a mouthful, it’s worse on paper: two separate, complicated forms that are confusing for customers and, the bureau contends, also burdensome for many mortgage servicers to fill out.

The goal is to replace them with a single, two-page document that clearly answers the questions: “Can I afford this mortgage?” and “Can I get a better deal somewhere else?”

Two of the potential designs for the new form each have a note at the top, in bold print: “You have no obligation to choose this loan. Shop around to find the best loan for you.”

The bureau’s other projects include improving transparency about credit card prices and fees, the exchange rates used for remittance transfers of money to other countries and the credit scores sold to consumers and creditors.

Using heatmaps and 13,000 clicks to understand pain points for mortgage disclosure? Data-driven government may have legs.

It’s not just the heatmaps: the CFPB reports that they read and analyzed the comments themselves. “There is symmetry here,” write the Web staff. “Heatmaps make it easier to understand and compare data. We want to improve disclosure so it is easier for consumers and lenders to understand and compare when they evaluate mortgage loans.”

As the newest .gov startup continues to scale, we’ll see if more experiments in open government design are given “freedom to fail,” a latitude that the father of the Internet, Vint Cerf, has hailed as an essential ingredient for government innovation. Stay tuned, and keep at eye on the CFPB.

Can technology be used to create a “21st Century regulator?” Keep an eye on Elizabeth Warren as she works to stand up the new Bureau of Consumer Financial Protection over the next months. As Bill Swindell reported for NextGov, the new consumer protection agency plans to use crowdsourcing to detect issues in the market earlier. In a world where studios can use tweets to estimate movie profits or researchers can use Twitter to predict the stock market, it makes sense for government to seriously examine data mining blogs and social networks to pick up the weak signals that predate real problems. Choosing to use such a methodology is applying a lesson from Web 2.0 for Gov 2.0.

This isn’t the first time the federal government has tried to use crowdsourcing for collaborative innovation in open government, certainly, but detecting consumer fraud in a networked world is such a massive challenge that the effort deserves special attention and scrutiny. What’s the thinking here? As Warren told Swindell:

“It’s also about how we will receive information about how the world works,” she said. “It’s about how people will tell us about what is happening. I want you to think about this more like ‘heat maps’ for targeted zip codes where problems are emerging, or among certain demographic groups, or among certain issuers,” Warren said in her still-not-decorated office.

How will crowdsourcing be focused? Swindell’s article provides more insight:

“The power of enforcement will be partly about the agency. But it will be partly, in the future, be about how people crowdsource around identified problems,” Warren said. “The idea that people can talk to each other, whether it’s through the agency or from other platforms. In a sense, the whole notion of how markets work will change.”

“In the old world, it would be up for the agency to come in, and you look very slowly through a sample of the banks to see what products they mailed out. And did they add a lot of fine print, nonsense by regulation that was not supposed to be there?[Now] all of the sudden you got information, and you got it much faster, and you have it more pinpointed and that becomes relevant for purposes of where you spend enforcement resources.”

I think the tools that can be at the new agency’s disposal will have at least three kinds of implications. First, information technology can help ensure that the new agency remains a steady and reliable voice for American families. The kinds of monitoring and transparency that technology make possible can help this agency ward off industry capture.

Second, technology can be used to help the agency become an effective, high-performance institution that is able to update information, spot trends, and deliver government services twenty-four hours a day, seven days a week. If we set it up right from the beginning, the agency can collect and analyze data faster and get on top of problems as they occur, not years later. Think about how much sooner attention could have turned to foreclosure documentation (robo-signers and fake notaries) if, back in 2007 and 2008, the consumer agency had been in place to gather information and to act before the problem became a national scandal.

And third, technology can be used to expand publicly available data so that more people can analyze information, spot problems, and craft solutions. When these data are made available – while also, of course, protecting consumer privacy, shielding personal information and protecting proprietary business information – a shared opportunity arises between the agency and people outside government to have a hand in shaping the consumer credit world.

When Elizabeth Warren meets with Silicon Valley executives, certain technologies are likely to be of particular interest. As reported, she’ll be talking with Hal Varian, Google’s chief economist. Varian is behind a “Google price index” created through online shopping data that measures inflation. For some perspective on his thinking and why leveraging big data is one of the most important trends in IT, watch the video from last year’s Gov 2.0 Summit below:

For more perspective on how big data is being put to work across government, academia and big business, check out the excellent Strata Week series at O’Reilly Radar. Data science is shaping up to be one of the key disciplines of the 21st Century. Whether it can be put to good use by government regulators is a question that will be fascinating to see answered.

UPDATE: Warren delivered a speech to the University of California at Berkeley during her trip where she elaborated further on her vision for the new consumer protection agency. Full text of the speech is embedded below. Selected quotes on data follow.

Technology may provide new tools for the media and government to determine what’s happening – but they can and are used against consumers. As is so often the case, technology is agnostic to the purpose it is bent towards.

Today, information is king—but information is not evenly accessed by all. Repeat players can understand a complicated financial product that the rest of us have difficulty parsing in full. Lenders can hire teams of lawyers to work out every detail of a contract, then replicate it millions of times; a consumer doesn’t have the same option. And with technology to keep track of every purchase, to watch every payment choice, to observe and record the rhythms of our lives, a sophisticated seller can harvest that information—sometimes in ways that provide value, but sometimes in ways that manipulate customers who will never see what happened to them.

Warren also talked about how technology can be used to connect the new regulator with consumers, with respect to a “virtual shingle.” We’ll all see how big those ears can be.

When an agency loses sight of the public it is designed to serve, academics say it has been captured. The new consumer agency can develop tools to help level the playing field and discourage capture. The American people can have not just one, but thousands of seats at the table. Even before the agency officially opens its doors, it can solicit information from the American people about the challenges and frustrations that they face with consumer financial products day in and day out—and it can organize that information and put it to good use. Data from the public can inform priorities, and it can signal problems both to consumers and businesses. Information technology can allow us to hang out a virtual shingle in front the Agency and to declare our intent to the world. It’s a lot harder to let yourself fail – and a lot easier for the public to hold you accountable – when you’ve transparently declared your mission and shared information the public can use to measure your success in meeting it. Technology can force this agency to remain true to its goals.

Warren also articulated her thoughts on a “data-driven agency” and empowering citizens “to help expose, early on, consumer financial tricks,” acting as a kind of collective digital neighborhood watch. It’s an interesting vision.

In a world of experts, it’s the experts that frame the questions to be asked, isolate the problems, sort through the data (if there are any), and try to design solutions—always with the industry looking on and chiming in. But we can do this differently.

A data driven agency won’t be about conventional wisdom. It will be about data. And those data should come from many sources—from financial institutions, from academic studies and from our own independent research. We can reinforce that approach by making sure that our analysts come from a diversity of backgrounds—finance, law, economics, sociology, housing.

But we can also gather data directly from the American people by asking them to volunteer to share with us the experiences they have with consumer credit products. We can open up our platform to families across the country who want to tell us what has happened to them as they have used credit cards, tried to pay off student loans, or worked to correct errors in a credit report. We can learn more about the loan application process, about what people see on the front end and what happens on the back end. We can learn about good practices, bad practices and downright dangerous practices, and we can report on the good, the bad and the ugly to increase transparency and to push markets in the right direction.

Normally, agencies use supervision and lawsuits to enforce the law. This agency will do that as the cop on the beat watching huge credit card companies, local payday lenders, and others in between. Technology can help us do that better, by making sure our enforcement priorities are tightly connected to the financial market realities as experienced by customers every day.

New technology can help us supplement the cop on the beat by building a neighborhood watch. The agency can empower a well-‐informed population to help expose, early on, consumer financial tricks. If rules are being broken, we don’t need to wait for an expert in Washington to wake up. If we set it up right from the beginning, the agency can collect and analyze data faster and get on top of problems as they occur, not years later. Think about how much sooner attention could have turned to foreclosure documentation (robo-‐signers and fake notaries) if, back in 2007 and 2008, the consumer agency had been in place to blow the whistle before the problem became a national scandal.

The agency may also be able to demonstrate how incentives can change when people are connected not only to the government, but also to each other. Through crowd-‐sourcing technology, consumers can deal collectively with those who would take advantage of them—and can reward those who provide excellent products and services. Imagine scanning a credit agreement and uploading to a website where software can analyze the text of the agreement. A consumer could help the agency spot new agreements on the market and customers could get more information as they make decisions. The new CARD Act requires credit card issuers to submit their agreements to the Federal Reserve for posting. That’s a model we can build on. Information – fast, accurate information from a variety of sources – has the power to transform the old measures of agency effectiveness.

Warren was also thoughtful about the risks and opportunities of using government data. She also alluded to the potential for entrepreneurs to develop apps to create something of value, an aspect of Gov 2.0 that has been widely articulated through the Obama administration’s IT officials.

As a researcher, I understand that data must always be handled carefully, and protection of personal data and proprietary models is paramount. But I also believe that better data, made available to the media, private investors, scholars and others, will, over time, produce better results. When data are widely shared, others can use those data to uncover new problems, to frame those problems in different ways, to propose their own public policy solutions, and, for the entrepreneurs in the group, to develop their own private apps to create something of value. I’ve seen some good ideas in my time, and I’ve learned that those ideas can come from unlikely places. I’m hopeful that, as we drive consumer credit markets toward working better for families, the new consumer agency will be smart enough to encourage – and then to build upon – good ideas that come from far outside the government sphere.

At 18F, Uncle Sam is hoping to tap the success of the U.K.’s Government Digital Services. If the new digital government team housed with the U.S. General Services Administration gets it right, they’ll succeed in building 21st century citizen services by failing fast instead of failing big, as the Center for Medicare and Medicaid Services memorably did last year with Healthcare.gov through poor planning and oversight and Social Security has this summer. One of the lessons learned from the Consumer Financial Protection Bureau‘s successful use of technology is to align open source policy with mission. This week, 18F has done just that, publishing an open source policy on Github that makes open source the default in development:

At 18F, Uncle Sam is hoping to tap the success of the U.K.’s Government Digital Services. If the new digital government team housed with the U.S. General Services Administration gets it right, they’ll succeed in building 21st century citizen services by failing fast instead of failing big, as the Center for Medicare and Medicaid Services memorably did last year with Healthcare.gov through poor planning and oversight and Social Security has this summer. One of the lessons learned from the Consumer Financial Protection Bureau‘s successful use of technology is to align open source policy with mission. This week, 18F has done just that, publishing an open source policy on Github that makes open source the default in development:

The question of

The question of