As the nation’s first startup agency in more than a generation, the Consumer Financial Protection Bureau has broken new ground in how it uses technology to create better Web products, publishes complaint data, shares software code, catalyzes innovation, uses the Internet to redesign forms, and, of course, regulates providers of consumer financial services. Now, it has floated a new proposal to create a consumer complaint database that would, for the first time, make the stories that consumers tell the regulatory agency public.

“The consumer experience shared in the narrative is the heart and soul of the complaint,” said CFPB Director Richard Cordray, in a statement. “By publicly voicing their complaint, consumers can stand up for themselves and others who have experienced the same problem. There is power in their stories, and that power can be put in service to strengthen the foundation for consumers, responsible providers, and our economy as a whole.”

The CFPB was given authority and responsibility for handling consumer complaints regarding financial services by the Dodd-Frank Wall Street Reform and Consumer Protection Act, more than three years ago. Today, the CFPB released an overview of the complaints that the agency has handled since July 21, 2011,

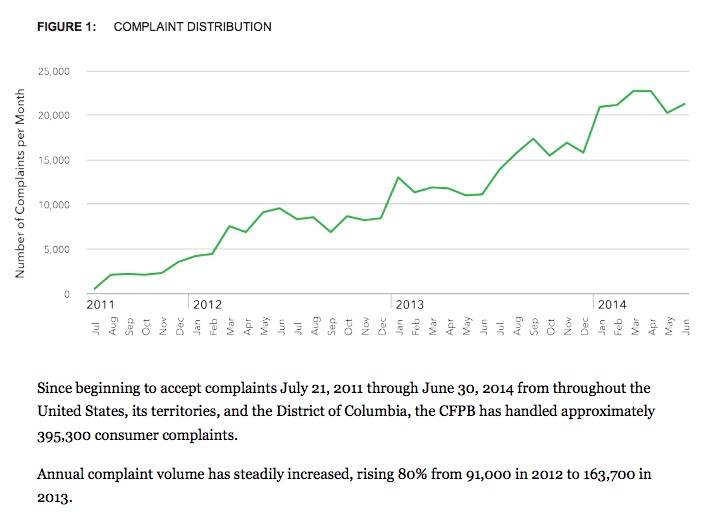

Today, the CFPB released an overview of complaints handled since the Bureau opened on July 21, 2011. (The graphics atop this post and below are sourced from this analysis.) According to the data inside, up until June 30, 2014, the CFPB has handled approximately 395,300 consumer complaints.

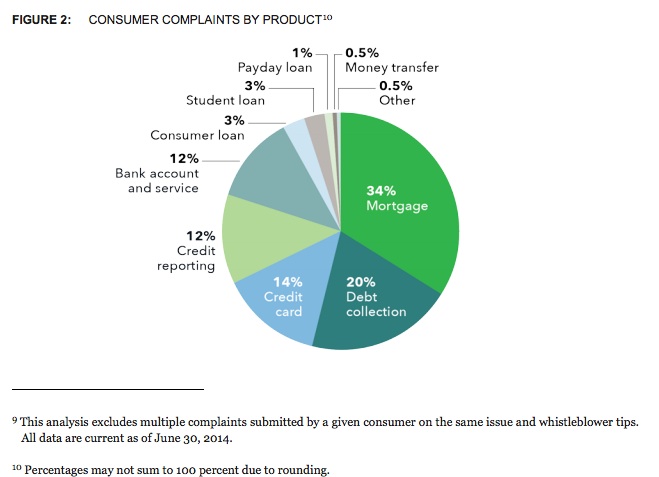

According to the overview, the World Wide Web has been a key channel for people to file complaints to the CFPB: 56% of all consumer complaints were submitted through the CFPB’s website. 10% were submitted via telephone calls, with the balance coming in through mail, email, and fax. The rest of the report contains tables and data that breaks down complaints by type, actions taken, company responses, and consumers’ feedback about company responses.

By releasing these narratives, not just the number of complaints, the agency holds that the following benefits will accrue: more context to the complaint, specific trends in complaints, enabling consumers to make more informed decisions, and spurring competition based on consumer satisfaction. In the release announcing the proposed policy, the CFPB emphasized that consumers must opt-in to share these stories: “The CFPB would not publish the complaint narrative unless the consumer provides informed consent. This means that when consumers submit a complaint through consumerfinance.gov, they would have to affirmatively check a consent box to give the Bureau permission to publish their narrative. At least initially, only narratives submitted online would be available for the opt-in.”

Consumers could subsequently decide to withdraw their consent, resulting in the regulator removing the complaint from their website. Companies will be given the opportunity to publish a written response to the complaints that would appear next to a given consumer’s story.

The agency’s proposal states that “no personal information will be shared, stating that “complaints would be scrubbed of information such as names, telephone numbers, account numbers, Social Security numbers, and other direct identifiers.”

Getting that right is important — watch for powerful financial companies, their lobbyists and sympathetic politicians to raise privacy concerns about the proposal in DC in the weeks to follow.

While it may not be apparent at first glance, however, the collection and publication of these complaints would have an important, tacit effect upon the market for financial services. By collecting, structuring and releasing consumer complaints as data, the CFPB could add crucial business intelligence into the marketplace for these services. This isn’t a novel model: the Consumer Product Safety Commission already discloses a public complaint database at SaferProducts.gov, enabling merchants and services like Consumer Products to give people crucial information about their purchases. The SEC and FINRA would be well-advised to release financial advisor data in a similar fashion. Someday, complaints submitted from mobile e-patients may have similarly powerful corrective effect in the market for health care goods and services.